If you’ve been watching mortgage rates tick higher over the past few weeks and wondering why, the answer lies not in what the Federal Reserve is doing — but in a corner of the bond market most Americans rarely think about: the 10-year U.S. Treasury note.

This past week, the 10-year yield surged to 4.687%, its highest reading since January 2025, before settling back near 4.61%. At the same time, the 30-year Treasury bond briefly topped 5.19%, a level not seen since before the 2008 financial crisis. The ripples have been immediate and painful for prospective homebuyers.

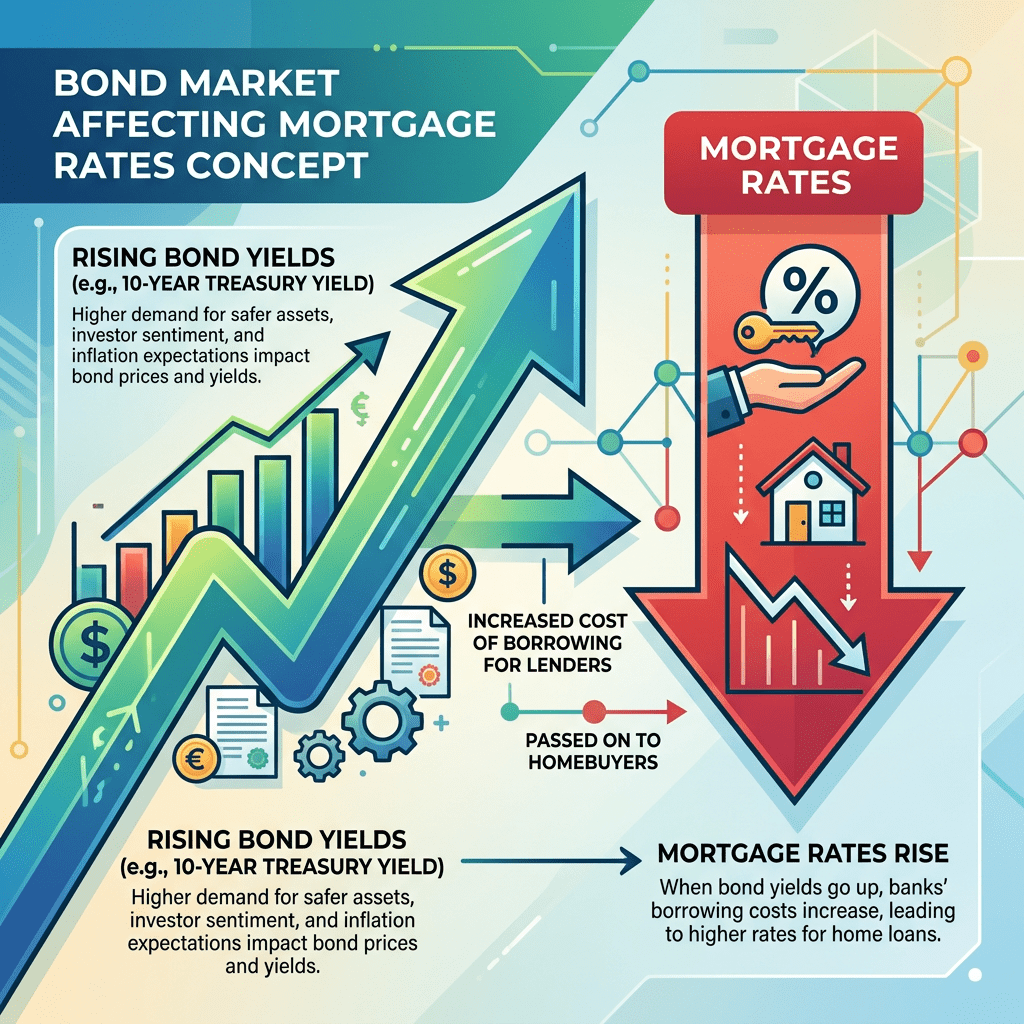

Why the 10-Year Treasury Drives Mortgage Rates

It’s a common misconception that the Fed directly sets mortgage rates. In reality, 30-year fixed mortgage rates are priced off the bond market — specifically the 10-year Treasury yield — not the federal funds rate. Mortgage lenders fund their loans by packaging them into mortgage-backed securities (MBS), which compete directly with Treasuries for investor capital. When Treasury yields rise, lenders must offer higher mortgage rates to attract buyers.

Where the 10-year Treasury yield moves, mortgage rates follow. The two are joined at the hip.

The “spread” between the 10-year Treasury and the average 30-year mortgage has historically run around 170–200 basis points. Today, with the 10-year near 4.6% and the 30-year fixed rate at 6.36%, that spread remains elevated — a sign that lenders are pricing in extra uncertainty around inflation and rate volatility.

Key Numbers at a Glance (May 2026)

| Instrument | Yield / Rate |

|---|---|

| 2-Year Treasury | 4.12% |

| 10-Year Treasury | 4.61% |

| 30-Year Treasury | 5.19% |

| 30-Year Fixed Mortgage (Freddie Mac) | 6.36% |

What’s Pushing Yields Higher?

The recent surge in long-dated Treasury yields is the product of several converging pressures. Geopolitical tensions — notably the conflict with Iran and its effect on oil prices and the Strait of Hormuz — have stoked inflation fears. Energy prices spiking above $100 per barrel earlier this month rattled bond investors who worry that sustained commodity inflation could force the Fed to keep rates elevated longer, or even hike again.

Adding to the pressure: minutes from the Fed’s most recent meeting revealed that most policymakers believe another rate increase could be warranted if inflation stays stuck above the 2% target. Markets are currently pricing in roughly a 40% chance of a 25 basis-point hike by December. New Fed Chair Kevin Warsh has also injected uncertainty into the outlook, with traders still calibrating their expectations to his approach.

The 30-year bond briefly touching 5.19% — a level last seen before the global financial crisis — underscores just how dramatically the rate environment has shifted from the near-zero world of 2020 and 2021.

The Real-World Impact on Homebuyers

The numbers translate directly into monthly pain. On a $500,000 home with a 20% down payment, a 30-year fixed mortgage at 6.36% carries a monthly principal and interest payment of roughly $2,494. At the 3% rates of 2021, that same loan cost about $1,686 per month — a difference of over $800 every month, or nearly $10,000 per year.

Mortgage applications have already shown signs of strain. In March, when rates previously spiked to a 5-month high of 6.43%, total applications plummeted 10.5% in a single week, with refinancing activity collapsing over 14% and purchase applications falling more than 5%.

What Could Bring Relief?

Some relief could come from unexpected quarters. Even as yields spiked mid-week, they fell sharply on Wednesday after President Trump signaled that negotiations with Iran were in their final stages — and three supertankers crossed the Strait of Hormuz with full cargoes. Oil prices retreated, inflation expectations cooled, and the 10-year yield pulled back from its 4.7% high toward 4.60%.

Most forecasters see mortgage rates remaining in the low-to-mid 6% range through the summer, with occasional volatility of 0.2–0.5% in either direction. Freddie Mac’s year-end 2026 forecast points to rates potentially declining to the high 5% range — but only if inflation data cooperates and the Fed can avoid further hikes.

What to Watch Next

- Iran ceasefire negotiations — a deal could quickly ease oil prices and Treasury yields

- Upcoming CPI and jobs data, which will signal whether the Fed needs to hike further

- Federal Reserve commentary from Chair Kevin Warsh on inflation tolerance

- The spread between 10-year Treasuries and 30-year mortgage rates — if it narrows, rates could ease even without a yield drop

For now, the bond market remains firmly in the driver’s seat. And until yields find a sustained lower footing, homebuyers will continue paying the price.

Leave a comment