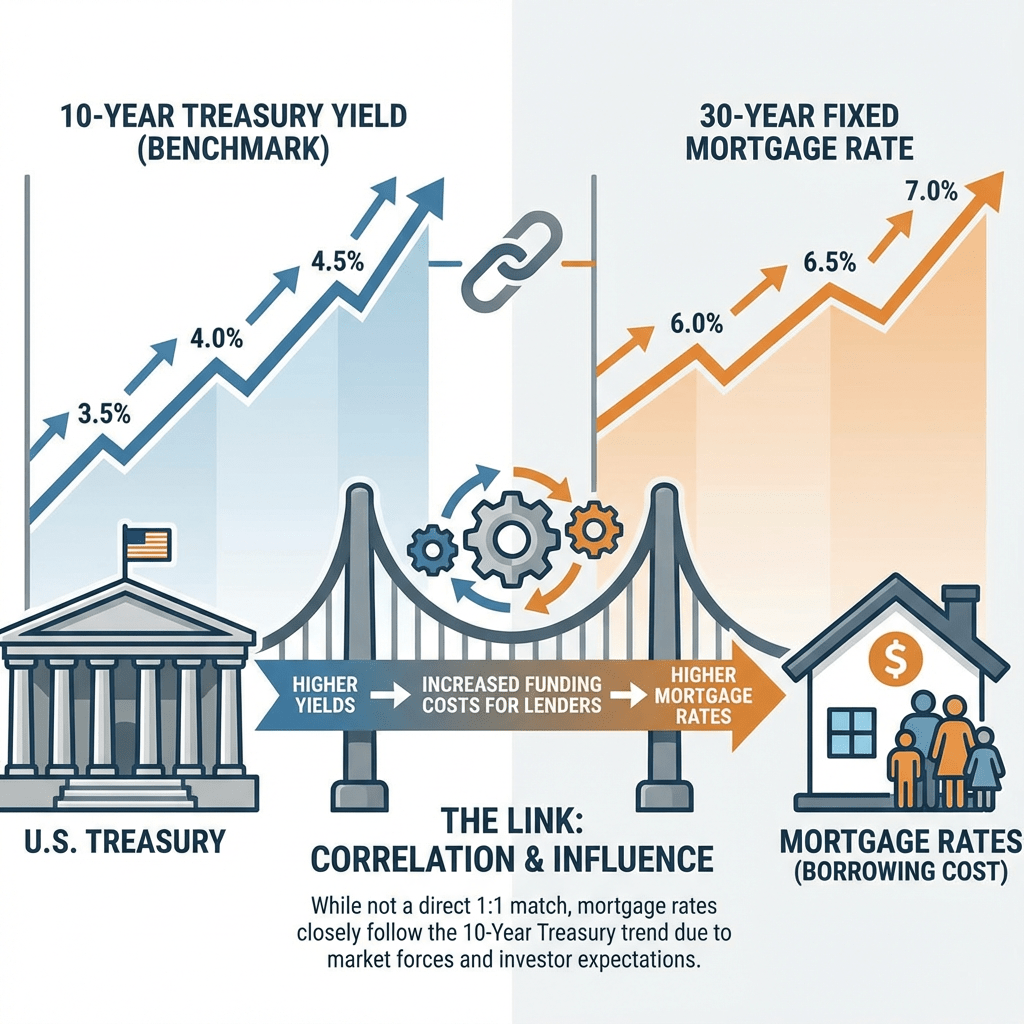

When markets react to war or geopolitical tension, they don’t directly move the 30‑year mortgage rate. Instead, they move a few key building blocks in the background. The most important is the yield on the 10‑year U.S. Treasury bond, which is the benchmark for long‑term interest rates. Lenders price 30‑year fixed mortgages at a spread above that 10‑year yield, adding in costs, risk, and profit. When the 10‑year goes up, mortgage rates usually follow; when it goes down, mortgage rates generally drift lower as well.

The Iran conflict matters because it has the potential to push oil prices higher and keep them elevated. Higher oil prices affect transportation, manufacturing, and shipping costs. These increased costs can push inflation higher. They can also prevent it from falling as quickly as the Federal Reserve would like. If inflation proves stubborn, the Fed is less likely to cut interest rates aggressively. That expectation alone can keep long‑term Treasury yields higher. As a result, 30‑year mortgage rates stay elevated for longer than the market anticipated just a few weeks ago.

Why the Market Shifted Back Above 6%

As we entered 2026, 30‑year fixed mortgage rates had finally moved closer to the 6% area. They had been stuck in the 7s for a long time. Many analysts were expecting a gradual move into the high‑5s as inflation cooled and the Fed prepared to ease policy. The outbreak of conflict with Iran changed the tone almost overnight. Traders reassessed the risk of higher oil prices and renewed inflation pressure. As a result, bond yields moved up, and mortgage‑backed securities sold off. This caused lenders to bump rate sheets back higher.

The result is that national averages for 30‑year conforming loans have moved back above 6% in the near term. We are not headed back to the extreme highs we saw before. The “easy” path lower rates has been interrupted. Instead of a smooth slide into the low‑5s, we’re more likely to see a choppy pattern. Rates will move up and down in response to economic data and geopolitical headlines. The bulk of 2026 will be spent somewhere around that 6% neighborhood.

What “Higher for Longer” Really Means for Borrowers

You’re going to hear the phrase “higher for longer” a lot. It’s important to understand what that means in practical terms. It does not necessarily mean a return to 7–8% 30‑year rates. Rather, it means that current levels will stick around longer than hoped. Any improvement is to be gradual instead of dramatic. Visualize a range where most of the movement occurs between the high‑5s and low‑6s. Occasionally, there are spikes above or dips below that range.

For home buyers, that translates into an environment where waiting for a huge drop could mean missing opportunities. In the current market, it’s important to stay informed and ready to act. If your plan depends on rates suddenly dropping, it has become less likely. A drop by more than a full percentage point quickly is not expected.

For existing homeowners, it means that a “refi boom” driven by a quick move to the low‑5s is less probable in the near term. However, targeted refinance opportunities will still appear. These opportunities will arise when the bond market has good days and rates temporarily improve.

How to Think About Locking vs. Floating

With geopolitical risks in play, rate volatility is to stay elevated. As a result, we will see 10-20 basis point swings in mortgage pricing over the course of a week. Sometimes these swings can even happen within a single day. In this type of market, having a clear lock strategy matters more than ever. If you’re under contract to buy a home, and your numbers work at today’s rate, it makes sense to lock. It is wiser to lock rather than gamble on short‑term moves driven by unpredictable headlines.

Floating can still be a practical choice. This is particularly true if you have a longer timeline. It also makes sense if there is flexibility in your purchase or refinance plans. Floating should be a strategic decision, not a default. Think in terms of “lock the payment that fits your budget.” Do not “chase the lowest possible rate.” If you can achieve a monthly payment that supports your financial goals, lock it in. This helps you reach those goals. It also protects you from the risks linked to geopolitical tension and inflation uncertainty.

Putting Today’s Rates in Historical Perspective

It’s easy to anchor on the ultra-low rates of the pandemic era. People feel disappointed by anything that starts with a “6.” But in a broader historical context, 30-year fixed rates in the 5–6% range are closer to normal than extreme. For decades, homeowners bought, sold, and built wealth in housing with rates higher than what we’re seeing today. The difference now is that home prices and payment expectations changed in the era of extremely cheap money. As a result, the mental adjustment is taking time.

Reframing today’s market as a return to more typical conditions can help both buyers and sellers make better decisions. Instead of asking, “When will rates get back to 3%?” ask this: “Does this home make sense for my long‑term plan?” Also, consider if the payment is reasonable if rates stay around this level. If the answer is yes, then geopolitical noise becomes less important. Short‑term rate moves matter less than your personal time horizon, job stability, and lifestyle goals.

Key Takeaways for Home buyers and Homeowners

First, expect volatility, not certainty. Headlines about conflict, inflation, and the Federal Reserve will continue to drive short‑term moves in mortgage rates. Second, plan around a realistic range rather than a specific rate number. For 30-year conforming loans, consider a band centered around 6%. This is a reasonable working assumption while the situation with Iran and energy prices unfolds. Third, focus on the monthly payment. Prioritize long-term affordability. Do this instead of trying to time the exact bottom of the rate cycle.

Finally, remember that you’re not locked into today’s rate forever. If you buy or refinance at current levels, and rates fall significantly later, you can choose to refinance again. This is, of course, assuming it aligns with your broader financial picture. Sensible expectations are crucial. Maintaining a clear budget is also important. Additionally, a flexible long‑term plan will serve you better than trying to react to every geopolitical headline in real time.

Leave a comment