Record numbers of Americans are draining their 401(k)s to stay in their homes — often without realizing there are far less costly alternatives.

Gregory Rutolo | NMLS #34860 | email gregory.rutolo@loanfactory.com

Something troubling is happening. It occurs at the intersection of two of America’s biggest financial crises. Most people aren’t connecting the dots.

Retirement hardship withdrawals are at an all-time high. Foreclosure filings are surging. In many cases, the same financially stressed homeowners are driving both statistics. They often make a short-term housing decision. This decision will cost them dearly in retirement.

If you work in financial planning, real estate, mortgage lending, or HR benefits, this article is for you. It is also applicable if you simply own a home and carry a 401(k).

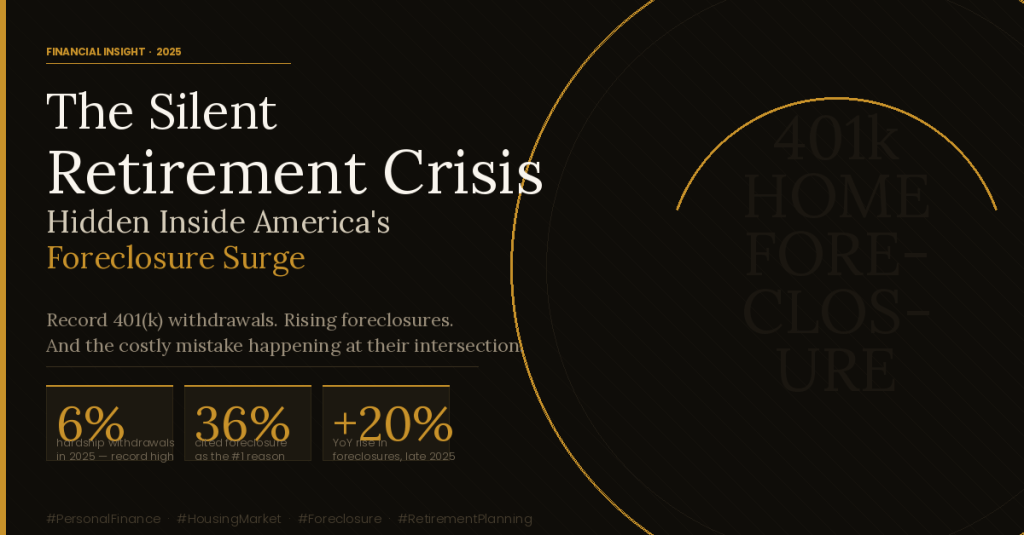

6% of retirement savers took a hardship withdrawal in 2025 — a record high

36% of those withdrawals were to prevent foreclosure or eviction

+20% year-over-year rise in foreclosure filings by late 2025

2% pre-pandemic average hardship withdrawal rate — now tripled

The Numbers Tell a Stark Story

Before the pandemic, roughly 2% of Americans with employer-sponsored retirement plans took hardship withdrawals in any given year. By 2025, that figure had climbed to 6%, setting a record. This signifies millions of households making a painful financial trade-off.

The single largest reason cited? Preventing foreclosure or eviction — accounting for 36% of all hardship withdrawals, ahead of even medical expenses. The median withdrawal size was $1,900, suggesting many of these aren’t large, planned distributions. They’re desperate, last-minute moves.

“People are not raiding their retirement accounts because they want to. They’re doing it because they feel they have no other choice.”The Hidden Cost of Waiting Too Long

Meanwhile, the housing picture has darkened considerably. Foreclosure filings had a modest dip in 2024. They then reversed sharply in 2025. They rose nearly 20% year-over-year by late in the year. Several factors drive this. Adjustable-rate mortgages are hitting their reset periods. Home insurance premiums have climbed over 60% since 2022 in some states. The general weight of inflation affects groceries, energy, and healthcare.

Why a 401(k) Withdrawal Is One of the Costliest Fixes

Tapping retirement savings to prevent foreclosure feels rational at first glance. You keep the house. You avoid a devastating credit hit. You move on. But the math is almost always brutal.

A hardship withdrawal is treated as ordinary income in the year it’s taken. For most middle-income earners, that means 22–24% going straight to federal taxes. If you’re under 59½ and don’t qualify for a penalty exception, add another 10% early withdrawal penalty. On a $20,000 withdrawal, you will net only $13,200. You would also permanently lose the decades of compounding growth that money would have generated.

Consider: $20,000 left in a 401(k) for 20 years at a 7% average return becomes roughly $77,000. That’s the real cost of the withdrawal — not $20,000, but closer to $64,000 in lost future wealth.

Alternatives Homeowners Should Exhaust First

The frustrating reality is that most homeowners facing foreclosure have options they either don’t know about or haven’t fully explored. Federal law requires mortgage servicers to work with borrowers before initiating foreclosure. Free housing counselors exist. Government programs have funds. Here’s how the alternatives stack up:

| Option | Financial Cost | Credit Impact | Retirement Impact |

|---|---|---|---|

| HUD Housing Counselor | Free | None | None |

| Loan Forbearance | Minimal | Minimal | None |

| Loan Modification | Low | Minimal | None |

| Homeowner Assistance Fund (HAF) | Free (grant) | None | None |

| HELOC / Home Equity Loan | Interest costs | None | None |

| Cash-Out Refinance | Closing costs | None | None |

| Short Sale | Lose home equity | Moderate hit | None |

| Chapter 13 Bankruptcy | Legal fees | Significant hit | None |

| 401(k) Hardship Withdrawal | Taxes + 10% penalty | None | Severe — permanent |

Nearly every choice ensures that retirement savings are left intact. This includes options that involve credit damage or losing the home. The 401(k) withdrawal is uniquely destructive. It harms your current financial situation after taxes and penalties. It also affects your future financial situation.

Action Steps — Before Touching Retirement Savings

- Call your loan servicer — ask specifically about forbearance, repayment plans, and loan modification. Servicers are legally obligated to discuss these options.

- Contact a HUD-approved housing counselor — free advice at 1-800-569-4287. They negotiate with lenders on your behalf at no cost.

- Check your state’s Homeowner Assistance Fund (HAF). These are federal relief funds distributed by states. Many still have money available for mortgage, insurance, and utility assistance.

- Explore a HELOC or cash-out refinance. If you still carry equity, borrowing against the home is almost always cheaper than a retirement withdrawal.

- Consult a bankruptcy attorney — Chapter 13 can instantly halt foreclosure proceedings and give you a structured repayment plan. A consultation is typically free.

The Bigger Picture We Can’t Ignore

America’s retirement savings shortfall was already one of the most consequential slow-moving crises in our economy. Tens of millions of workers reach retirement age with little or nothing saved. The households now making hardship withdrawals are disproportionately those who were already behind. Each withdrawal widens that gap further.

Foreclosures, even at today’s elevated pace, stay far below the catastrophic levels of 2010. Yet, the directional trend is up nearly 20% year-over-year. Adjustable-rate resets and insurance cost escalation are still working through the process. This suggests pressure that isn’t going away soon.

For financial professionals, this is a moment to be proactive. Clients who hold retirement accounts and carry mortgages need a conversation before they make a withdrawal, not after. The window to act is limited. People must choose a better path quickly. Once someone is 90 days past due, they face formal proceedings.

The retirement savings gap in this country is already a crisis. Draining what little people have saved to stay housed worsens the structural situation. It is detrimental for individuals and affects all of us.The Long View

If you found this useful, share it with someone in your network. That person could work in lending, real estate, benefits administration, or financial planning. The people most at risk of making this mistake often don’t know the alternatives exist — until it’s too late.

The most expensive financial decision isn’t always the one that feels the most desperate at the moment. Instead, it’s the one whose true cost only becomes visible years later.

Leave a comment